A critical question for your portfolio and where to look for winners today

In the mid-1980s, the technology sector stood at a precipice that mirrors the structural shifts currently observed in the global financial markets. At the center of this historical pivot was Intel, a company that had built its reputation and fortune on the production of memory chips. By 1985, however, the firm’s foundational business was under existential threat from Japanese competitors who were aggressively undercutting prices and eroding profit margins. During this period of intense volatility, Intel president Andy Grove posed a transformative hypothetical question to co-founder Gordon Moore: "If the board fired us and brought in a new CEO, what would he do?"

The subsequent realization was both stark and uncomfortable. A new leader, unburdened by the emotional attachment to the company’s legacy as a memory manufacturer, would immediately exit the declining memory market. Despite memory chips being synonymous with Intel’s identity, Grove and Moore recognized that clinging to the past was a recipe for obsolescence. They made the strategic decision to pivot toward microprocessors, a move that required shifting massive amounts of capital, talent, and focus. This repositioning did not signal a retreat but rather an aggressive pursuit of a new, high-growth frontier. This decision laid the technical and economic groundwork for Intel’s multi-decade dominance of the personal computer era.

The Modern Market Context: A Transition to Neutrality

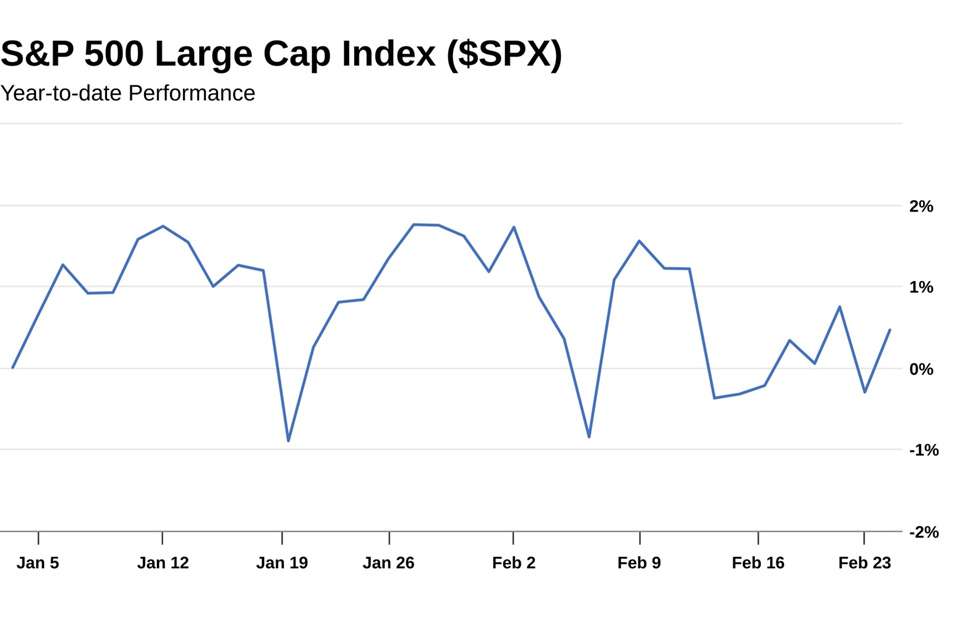

As of early 2026, the broader equity markets appear to be facing a similar crossroads. Following a three-year period of exceptional growth, the S&P 500 has entered a phase of relative stagnation, posting gains of less than 1% for the current year. This follows a period of significant appreciation: the index rose by 24% in 2023, 23% in 2024, and 16% in 2025.

For many investors, the current "sideways" movement of the market is a source of frustration. However, market analysts suggest that this period of neutrality is not necessarily a precursor to a downturn, but rather a symptom of a significant internal rotation. Much like Intel in the 1980s, the market is currently grappling with the transition from yesterday’s high-fliers to tomorrow’s essential infrastructure. The primary challenge for contemporary portfolio managers is to distinguish between a "risk-off" environment—where capital flees the market—and a "rotation" environment, where capital moves from overextended sectors into emerging areas of value.

The Two-Phase Evolution of the AI Revolution

The current market rotation is most visible within the artificial intelligence (AI) sector. Experts divide technological revolutions into two distinct stages: the visibility phase and the infrastructure phase.

The first phase, which dominated market headlines and returns from 2023 through 2025, was characterized by consumer-facing applications and high-profile software breakthroughs. This era was defined by the rapid adoption of large language models (LLMs) and the "flashy" side of generative AI. During this period, companies that could demonstrate immediate AI integration saw their valuations soar as investors chased the "first-mover" advantage.

The market has now entered the second phase: the infrastructure layer. This stage is less about the software interface and more about the physical and technical foundations required to sustain AI at scale. This transition is evidenced by a massive shift in corporate capital expenditure (CapEx). The world’s largest technology firms—including Microsoft, Amazon, Meta, and Alphabet—are collectively deploying hundreds of billions of dollars toward the construction of data centers, the procurement of advanced semiconductors, and the reinforcement of electrical grids to power these energy-intensive systems.

Chronology of Infrastructure Scaling

The move toward infrastructure is not merely theoretical; it is reflected in recent large-scale industrial projects. In late 2025 and early 2026, Elon Musk’s xAI project in Tennessee became a focal point for this shift, linking together 100,000 GPUs to create one of the world’s most powerful supercomputers. This project represents a broader trend where the "Magnificent Seven" and other tech titans are shifting their focus from software experimentation to the physical realities of compute power.

- 2023-2024: Peak hype for generative AI applications; massive retail investment in software-heavy AI firms.

- Mid-2025: Market starts to plateau as investors question the immediate ROI of AI software.

- Late 2025 – Early 2026: Significant capital rotation into "hard" AI assets, including energy providers, specialized networking hardware, and cooling systems.

- Present: The S&P 500 shows minimal growth as capital exits "Phase 1" winners and seeks entry points in "Phase 2" infrastructure providers.

Supporting Data: The Cost of Intelligence

The financial requirements for this second phase are unprecedented. According to recent quarterly filings, the combined CapEx of the leading four "hyperscalers" (Amazon, Google, Microsoft, and Meta) has reached a run rate exceeding $150 billion annually. This spending is directed toward several key sub-sectors:

- High-Performance Computing (HPC): The demand for advanced chips remains high, but the focus has expanded to include the specialized motherboards and interconnects that allow thousands of chips to work in unison.

- Energy and Utilities: AI data centers are estimated to require significantly more power than traditional facilities. This has led to a resurgence in interest in nuclear energy and grid modernization stocks.

- Connectivity and Transmission: As data workloads expand, the "connective tissue" of the internet—wireless and video communication protocols—must be upgraded to handle increased throughput with lower latency.

Case Study: The Role of InterDigital (IDCC)

In this environment of rotation, analysts such as Louis Navellier point to companies like InterDigital (IDCC) as examples of "infrastructure-adjacent" winners. InterDigital does not build chatbots; instead, it develops the foundational wireless and video communication technologies that enable high-performance systems to function.

As AI workloads move from centralized servers to "edge" devices (such as smartphones and localized hardware), the demand for efficient data transmission protocols increases. InterDigital’s financial health reflects this demand, with year-over-year sales increasing by 28%. From a quantitative perspective, the company currently maintains a high "B" rating in financial strength and growth momentum. This suggests that while the broader market may be flat, companies providing the essential underlying technology for AI scaling continue to see robust fundamental growth.

Official Responses and Analyst Perspectives

Market strategists suggest that the current environment requires a "CEO mindset" regarding portfolio management. Quantitative investment firm Navellier & Associates has reportedly repositioned hundreds of millions of dollars in response to these trends. Louis Navellier, the firm’s founder, has emphasized that the "easy gains" from early AI software names have likely been realized, and the next leg of growth will be found in companies with superior financial strength that provide the "picks and shovels" for the AI era.

"The biggest mistake in a rotating market isn’t moving too soon; it’s waiting too long to acknowledge that the leadership has changed," Navellier noted in a recent analysis. This sentiment is echoed by institutional traders who observe that while the S&P 500 appears stagnant on the surface, there is intense buying activity in sub-sectors related to power, cooling, and specialized networking hardware.

Broader Impact and Implications for the Future

The shift from applications to infrastructure has several long-term implications for the global economy. First, it underscores the "physicality" of the digital revolution. The demand for AI is driving a massive industrial build-out that resembles the expansion of the railroads or the electrical grid in previous centuries. This has a "multiplier effect" on industries that were previously considered stagnant, such as heavy electrical equipment manufacturing and specialized real estate (Data Center REITs).

Second, the current market rotation serves as a reminder of the importance of "unemotional" investing. Just as Intel had to abandon its identity as a memory company to survive, modern investors may need to move away from the "darling" stocks of the last three years to capture the next wave of growth.

The question originally posed by Andy Grove remains the most pertinent tool for navigating today’s financial landscape. If an investor were to "fire themselves" and look at their holdings with the cold, objective eye of a new manager, they would likely find that many of their current positions are based on yesterday’s breakthroughs rather than tomorrow’s necessities. The transition to AI Phase 2 is not a signal of the end of the AI boom, but rather a maturation process where the focus shifts from what AI can say to how the world will physically support what AI can do. For those willing to rotate, the current neutral market is not a wall, but a doorway to a more disciplined and fundamentally sound investment strategy.