The Economic Logic and Long-Term Projections of the $710 Billion Artificial Intelligence Infrastructure Buildout

The global financial landscape is currently defined by a massive divergence in perspective regarding the capital expenditure strategies of the world’s largest technology firms. As of early 2025, the five primary hyperscalers—Microsoft, Amazon, Alphabet, Meta, and Oracle—have collectively committed approximately $710 billion toward artificial intelligence (AI) infrastructure this year. This expenditure, which averages nearly $2 billion per day, is being directed into high-performance compute clusters, specialized data centers, fiber-optic networks, and advanced cooling systems. While critics suggest this represents the most significant capital misallocation since the dot-com bubble of 1999, a detailed economic analysis of the three primary revenue engines of AI suggests a potential for historic returns on invested capital (ROIC) that could redefine corporate profitability in the coming decades.

The Scale of Modern AI Capital Expenditure

The $710 billion figure represents a fundamental shift in corporate strategy, moving away from software-as-a-service (SaaS) maintenance toward a massive physical buildout. This capital is predominantly allocated to the procurement of graphics processing units (GPUs), the construction of specialized power-dense data centers, and the securing of energy resources required to run large-scale inference and training models.

The skepticism from Wall Street stems from the "funding gap" between current infrastructure spend and immediate revenue generation. However, proponents of the current spending levels argue that the hyperscalers are not merely buying equipment but are building a new utility layer for the global economy. This layer is designed to support three distinct revenue vectors: consumer subscriptions, enterprise knowledge work automation, and physical robotics.

A Chronology of the AI Investment Cycle

The current investment cycle can be traced back to the public release of large language models (LLMs) in late 2022, which sparked a corporate arms race for compute capacity.

- Phase I (2022–2023): Proof of Concept. Companies focused on model training and basic chatbot integration. Capital expenditure was significant but primarily focused on research and development.

- Phase II (2024–Present): The Infrastructure Surge. Realizing that model performance scales with compute, the "Big Five" shifted to massive physical expansion. This phase is characterized by the acquisition of specialized hardware and the development of proprietary energy solutions.

- Phase III (Expected 2026–2030): The Application and Platform Era. This future phase involves the transition from infrastructure providers to platform owners, where revenue is generated through widespread enterprise adoption and autonomous systems.

The Three Revenue Engines Powering the AI Economy

To justify a $700 billion annual expenditure, the resulting markets must operate at a scale previously unseen in the technology sector. Economic modeling identifies three primary pillars for these returns.

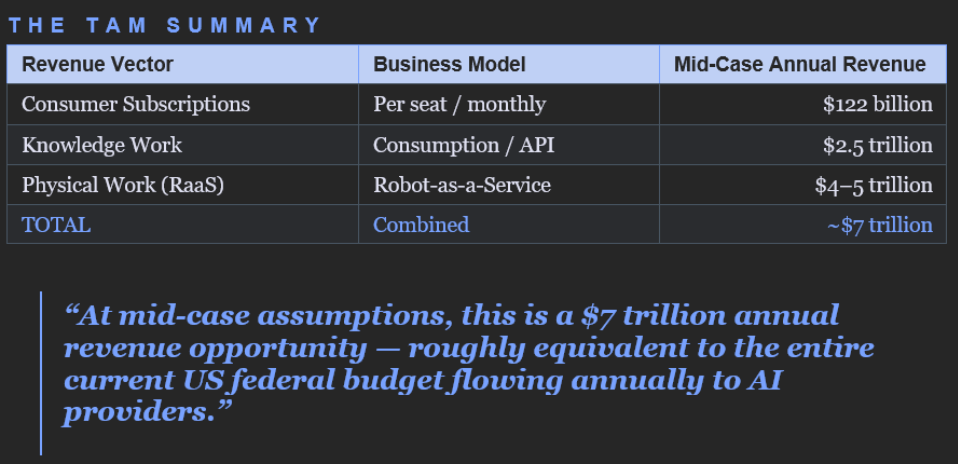

Consumer AI Subscriptions: The Entry Point

Consumer-facing AI represents the most immediate revenue stream. Currently, services such as ChatGPT Plus, Gemini Advanced, and Claude Pro have established a subscription-based model ranging from $20 to $30 per month.

Market analysis suggests an addressable global base of approximately 3.5 billion consumers, excluding those below viable income thresholds. Based on tiered global pricing—accounting for $25 ARPUs in developed markets and lower rates in emerging economies—a 625 million subscriber base could generate roughly $120 billion in annual revenue. While substantial, this "base layer" is considered the smallest of the three projected revenue engines.

Enterprise AI and Knowledge Work Automation

The second and more significant engine is the automation of knowledge work. There are approximately 560 million knowledge workers globally, including analysts, engineers, marketers, and legal professionals. The total global labor cost for this cohort is estimated at $32 trillion annually.

The shift in the business model here is critical: moving from "per-seat" software pricing to "consumption-based" value capture. If AI systems can automate 40% of knowledge work tasks and vendors capture 20% of that created value, the annual revenue potential reaches approximately $2.56 trillion. This model anchors revenue against total labor budgets rather than traditional software budgets, which are historically 10 to 50 times smaller.

Physical AI and Robotics: The Robotics-as-a-Service Model

The largest long-term opportunity lies in physical labor. With 3 billion physical workers globally in manufacturing, logistics, and healthcare, the total global labor cost exceeds $39 trillion.

The emerging commercial model is "Robot-as-a-Service" (RaaS), where enterprises lease integrated hardware and software systems. For this market to reach maturity, humanoid robotics must follow a hardware cost curve similar to solar panels or lithium-ion batteries. Industrial robot arms that cost $100,000 twenty years ago can now be deployed for under $30,000. If humanoid units reach a price point of $15,000 to $20,000, the addressable market for physical automation is projected to reach $4 trillion to $5 trillion annually over a 20-year horizon.

Comparative Analysis of Margins and ROIC

Profitability in the AI sector is expected to vary significantly across these three vectors. Consumer AI, being a pure software play, is projected to maintain operating margins of 50% to 60%. Enterprise knowledge work, which requires higher compute intensity, may see margins of 35% to 45%. Physical robotics, involving maintenance and depreciation of hardware, is modeled at 20% to 30%.

When blended across a projected $7 trillion total addressable market (TAM), the resulting operating margin is estimated at 32%. After accounting for corporate taxes, this would generate approximately $1.77 trillion in annual after-tax operating profit.

To put this in perspective:

- Total S&P 500 Annual Earnings: ~$1.5 trillion.

- Projected AI Maturity Earnings: ~$1.77 trillion.

Based on a cumulative net invested capital of $6.4 trillion over 20 years, the ROIC at maturity is calculated at 27% to 28%. This would place AI infrastructure in the same tier of capital efficiency as Alphabet (25-30%) and Microsoft (35-40%), and significantly above the 8% to 10% returns typically seen in traditional industrial or utility sectors.

The "J-Curve" and Near-Term Market Volatility

Despite the long-term potential, the "J-curve" effect is creating significant short-term anxiety in public markets. The J-curve describes the period where capital is being consumed far faster than it is being returned.

Current estimates suggest that the industry’s ROIC may not cross the 12% cost-of-capital threshold until year nine or ten of the buildout. This "funding gap" is already causing stress in certain areas of the market, particularly for entities relying on expensive private credit to fund infrastructure. Recent redemption pressures at large private credit vehicles underscore the risks for over-leveraged, pure-play infrastructure borrowers.

However, the hyperscalers—Microsoft, Amazon, Meta, and Alphabet—are uniquely insulated from this pressure. These firms generate between $60 billion and $100 billion in free cash flow annually from their core businesses (Search, AWS, Advertising, Office 365), allowing them to fund the J-curve internally without external debt or equity dilution.

Geopolitical Context and Official Sentiment

The decision to maintain high capex levels is increasingly influenced by national security and geopolitical competition. The emergence of high-performance models from international competitors, such as China’s DeepSeek R1, has reframed the AI race as a strategic imperative rather than a purely commercial one.

Hyperscaler executives have consistently signaled that the risk of under-investing is greater than the risk of over-investing. During recent earnings calls, the prevailing sentiment among CEOs is that the first companies to achieve Artificial General Intelligence (AGI) or near-AGI capabilities will possess an unassailable competitive advantage. In this context, the $700 billion annual spend is viewed as a "call option" on a technological discontinuity that would render traditional financial models obsolete.

Broader Implications for the Global Economy

The transition from AI infrastructure to AI platforms represents the next phase of wealth creation. Historically, during the internet era, infrastructure providers like Cisco and Intel saw early gains, but the most significant long-term value was captured by platform companies like Google, Meta, and Netflix.

The current data suggests that the "Big Five" are attempting to occupy both roles simultaneously. By owning the data centers (infrastructure) and the foundational models (platform), they aim to capture the lion’s share of the projected $7 trillion annual revenue.

For the broader economy, this buildout implies a massive increase in demand for energy and specialized real estate. Data center REITs and power infrastructure providers are becoming critical components of the AI supply chain, benefiting from the hyperscalers’ commitment to long-term spending regardless of short-term stock market fluctuations.

Conclusion: The Path Toward Maturity

While the $710 billion annual expenditure by Big Tech appears staggering, it is grounded in a logical expansion of the total addressable market for labor. By moving from software budgets to labor budgets, the ceiling for technology revenue has effectively risen by an order of magnitude.

The current market "choppiness" reflects the uncomfortable reality of the J-curve, where the costs are visible today but the $1.77 trillion in annual profits remains years in the future. Nevertheless, for firms with the balance sheet strength to survive the funding gap, the projected 28% ROIC suggests that the current era of "lighting money on fire" may eventually be remembered as one of the most productive capital allocation cycles in modern corporate history.