Market Volatility and Federal Reserve Policy Amid Geopolitical Uncertainty and Shifting Economic Indicators

The Federal Open Market Committee (FOMC) concluded its highly anticipated March meeting this week, electing to maintain the federal funds rate at its current range of 3.5% to 3.75%. This decision marks the second consecutive meeting where the central bank has opted for a pause, reflecting a cautious "wait-and-see" approach amidst a rapidly shifting global economic landscape. While the decision to hold rates steady was widely expected by institutional analysts, the underlying data and the internal dissent within the committee suggest a growing fragmentation in the consensus that has defined monetary policy over the last several quarters. As the "March Madness" of the college basketball season unfolds on the court, a parallel level of unpredictability is manifesting in the global markets, driven by a collision of cooling domestic inflation, a softening labor market, and a sudden spike in geopolitical tensions that has sent energy prices to multi-month highs.

The FOMC Decision and Internal Dissent

The Federal Reserve’s decision to maintain the status quo was not reached with the usual level of unanimity that has characterized the tenure of Chair Jerome Powell. In an 11-to-1 vote, Fed Governor Stephen Miran broke ranks with the majority, advocating for a 25-basis-point rate cut. This dissent is significant, as it represents the first public fracture in the Fed’s united front in recent months and underscores a burgeoning debate within the central bank regarding the timing of a pivot toward monetary easing. Miran’s push for a cut likely stems from concerns over the cooling labor market and the potential for restrictive rates to overcorrect an economy that is already showing signs of fatigue.

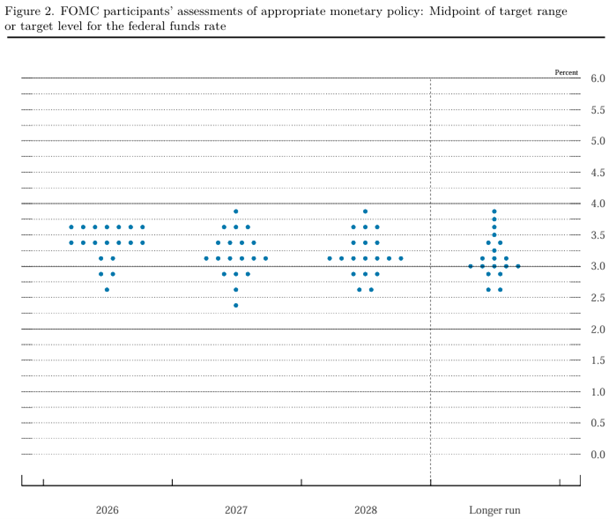

The Fed’s updated "dot plot," a visual representation of where individual policymakers expect interest rates to be in the future, further illustrated this internal divide. The survey revealed a wide dispersion of expectations: while a portion of the committee still anticipates multiple rate cuts before the end of the year, a growing hawkish contingent remains skeptical, with some officials projecting no cuts at all if inflation proves to be "sticky." The FOMC’s official statement reflected this ambiguity, noting that while economic activity has been expanding at a "solid pace," the implications of ongoing developments in the Middle East remain "uncertain" and pose a potential risk to the domestic outlook.

A Chronology of Shifting Economic Expectations

At the outset of the year, the prevailing narrative among economists and market participants was one of a "soft landing." The script was relatively straightforward: inflation was on a clear downward trajectory, economic growth remained resilient, and the Federal Reserve was poised to begin a cycle of rate reductions as early as the first half of the year. Throughout January and much of February, the data largely supported this optimistic view.

However, the timeline of stability began to unravel in late February and early March. The initial catalyst was a series of hotter-than-expected manufacturing and producer price reports, followed by a sharp escalation in geopolitical conflict in the Middle East. These events have introduced a "second wave" of inflation fears just as the central bank was preparing to declare victory over the first. The transition from a predictable path to one characterized by volatility has left investors re-evaluating their portfolios, as the traditional "top seeds" of the market—large-cap equities and interest-rate-sensitive bonds—face new headwinds.

The Inflation Divergence: CPI vs. PPI

The complexity of the current economic environment is perhaps best illustrated by the divergence between consumer and producer price indices. The latest Consumer Price Index (CPI) report, released earlier this month, appeared to offer a sigh of relief. Headline inflation rose by 0.3% in February, bringing the year-over-year increase to 2.4%, a figure that aligned perfectly with consensus forecasts. Core CPI, which strips out the volatile food and energy sectors, also met expectations, suggesting that the underlying "disinflationary" trend remained intact. Crucially, shelter costs, which have been a primary driver of service-sector inflation, showed signs of easing, providing hope that the Fed’s target of 2% was within reach.

However, the subsequent Producer Price Index (PPI) report told a different story. The PPI, which measures inflation at the wholesale level and often serves as a leading indicator for future consumer prices, surged by 0.7% in February. This was more than double the forecast of most private-sector economists. The internal components of the PPI were particularly concerning: wholesale food prices saw a significant uptick, and prices for finished goods jumped by 1.1%. These figures suggest that inflationary pressures are still bubbling beneath the surface of the supply chain, threatening to pass through to consumers in the coming months. This "stuck between a rock and a hard place" scenario is what prevented the Fed from adopting a more dovish tone during this week’s meeting.

Softening in the Labor Market

While inflation remains the Fed’s primary focus, the "maximum employment" half of its dual mandate is now demanding equal attention. For the first time in this tightening cycle, the labor market is showing unambiguous signs of cooling. The February jobs report revealed a loss of 92,000 jobs, marking the third time in five months that payrolls have declined. Furthermore, the national unemployment rate has ticked higher to 4.4%, a level that historically has preceded more significant economic slowdowns.

During his post-meeting press conference, Chair Powell acknowledged these vulnerabilities, specifically noting that private-sector job creation has stalled. The Fed’s recognition of labor market weakness is a pivotal shift in rhetoric. Previously, the "tight" labor market was cited as a reason to keep rates high to prevent a wage-price spiral. Now, the softening of the employment sector provides a compelling argument for rate cuts to prevent a recession, even as the PPI data suggests that the fight against inflation is not yet over.

The Geopolitical Shock and Energy Markets

Adding to the Fed’s dilemma is the sudden and sharp rise in energy costs. The escalating conflict in the Middle East has disrupted global shipping lanes and heightened concerns over regional oil production. As a result, crude oil prices have broken above the $100-per-barrel threshold, a psychological and economic level that typically triggers a contraction in consumer discretionary spending. Gasoline prices have followed suit, reaching their highest levels in months.

Energy prices act as a regressive tax on the economy, increasing the cost of everything from home heating to the transportation of groceries. For the Federal Reserve, rising oil prices represent a "supply-side shock" that they cannot control with interest rate policy. If the Fed cuts rates to support the weakening labor market, they risk fueling inflation that is already being pushed higher by energy costs. If they keep rates high to fight energy-driven inflation, they risk deeper job losses and a potential hard landing. This geopolitical "wildcard" has effectively dismantled the predictable economic script of early 2026.

Broader Impact and Market Implications

The confluence of these factors—divergent inflation data, a weakening job market, and soaring energy prices—is reshaping the investment landscape. Analysts suggest that the era of relying on broad market indices may be giving way to a period where "stock picking" and sector-specific themes become paramount. While the "top seeds" of the market remain fixated on the Fed’s every word, a significant shift in capital is occurring toward infrastructure and technological buildouts that are less sensitive to short-term interest rate fluctuations.

One of the most prominent emerging themes is the massive investment in artificial intelligence (AI) and the physical infrastructure required to sustain it. Regardless of whether the Fed cuts rates in June or September, the demand for data centers, power generation, and advanced semiconductors continues to accelerate. Furthermore, the increase in global instability has led to a renewed focus on national defense and global security systems, creating a tailwind for companies involved in aerospace and defense technology.

Fact-Based Analysis of the Path Forward

Looking ahead, the Federal Reserve remains in a precarious position. The next several months of data will be critical in determining whether the February PPI spike was an anomaly or the start of a trend. If energy prices remain above $100 per barrel, the Fed may find it impossible to cut rates without risking a resurgence of headline inflation. Conversely, if the unemployment rate continues its upward trajectory toward 5%, the political and economic pressure to ease monetary policy will become overwhelming.

Market participants are currently pricing in a high probability of a rate cut by the June FOMC meeting, but those expectations are increasingly fragile. The "Cinderella stories" of the current market—overlooked companies in the energy, infrastructure, and AI-support sectors—may continue to outperform the broader market as they provide a hedge against both inflation and economic stagnation. In this environment, the traditional "brackets" of investment strategy are being rewritten, and the ability to distinguish between temporary noise and structural shifts in the economy has never been more vital for maintaining capital stability. For now, the "madness" in the global economy appears set to continue well beyond the month of March, as the Federal Reserve navigates one of the most complex policy environments in its modern history.