Energy Price Volatility and Persistent Inflationary Pressures Challenge Federal Reserve Policy Objectives Amid Geopolitical Instability

The contemporary American economic landscape is increasingly defined by a resurgence of energy price volatility that evokes memories of the 1970s, a period when long lines at gas stations became a visceral symbol of rampant inflation. While the current economy has not yet returned to the structural dysfunction of that era, the recent trajectory of energy costs is providing a stark reminder to investors and policymakers of how rapidly geopolitical tensions can destabilize domestic price stability. According to data provided by AAA, the national average for a gallon of regular gasoline has undergone a significant ascent, climbing from $2.98 on February 26 to approximately $4.16 in April. This sharp increase occurs against a backdrop of deteriorating diplomatic conditions in the Middle East, where a fragile ceasefire between regional powers appears to be faltering, leading to heightened anxiety in global oil markets.

The significance of rising energy costs extends far beyond the immediate financial burden placed on motorists at the pump. In a modern interconnected economy, energy serves as a primary input for virtually every sector. Increased fuel costs inevitably permeate the supply chain, manifesting in higher shipping rates, elevated airfares, and increased production costs for agricultural products. Consequently, the recent surge in petroleum prices is viewed by economists as a leading indicator of broader inflationary pressures that may soon be reflected in the prices of everyday consumer goods and services. As market participants scrutinize the latest economic releases, the focus has shifted toward the sustainability of the Federal Reserve’s current monetary policy and the likelihood of achieving the elusive "soft landing."

The Divergence of Inflation Indicators: PCE and CPI Data Analysis

To understand the current inflationary environment, it is essential to examine the two primary metrics utilized by the U.S. government: the Personal Consumption Expenditures (PCE) price index and the Consumer Price Index (CPI). These reports offer a comprehensive, albeit retrospective, view of how price pressures are evolving.

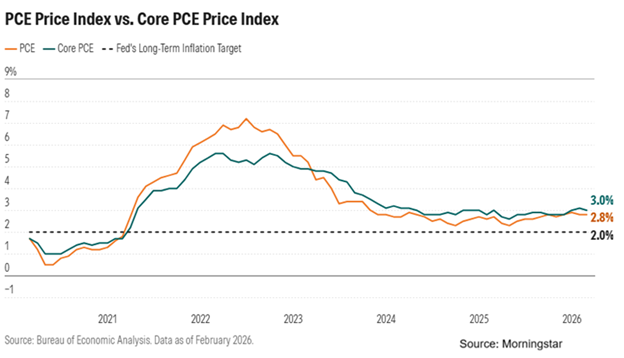

The PCE price index, which serves as the Federal Reserve’s preferred gauge for tracking inflation due to its ability to account for changes in consumer behavior, recently indicated that headline inflation rose by 0.4% in February. On a year-over-year basis, the PCE stands at 2.8%, a figure that aligns with consensus expectations but remains stubbornly above the Federal Reserve’s long-term target of 2%. The "core" PCE, which excludes the volatile categories of food and energy to provide a clearer view of underlying trends, also rose by 0.4% for the month, reaching a 3.0% year-over-year increase. These figures suggest that even before the full impact of the recent energy price spike was felt, inflationary pressures remained deeply embedded in the service sector and housing market.

The Consumer Price Index (CPI) report for March provided a more immediate reflection of the energy sector’s impact. Headline CPI surged by 0.9% for the month, marking the most significant monthly increase since 2022. Within this report, the energy component was the primary driver, soaring by 10.9%. Specific sub-categories showed even more dramatic increases: gasoline prices jumped by 18.9%, while fuel oil prices experienced a staggering 44.2% surge. Despite these headline-grabbing numbers, the core CPI—which strips out energy and food—increased by a more modest 0.2% in March and 2.6% over the past 12 months. This divergence highlights a critical reality for the Federal Reserve: while core inflation shows signs of gradual cooling, the volatility of energy prices threatens to pull the headline figure upward, potentially unanchoring inflation expectations among the public.

Chronology of Geopolitical Escalation and Market Impact

The current spike in energy costs can be traced through a specific timeline of geopolitical events that began in late February and accelerated through the spring.

- February 26: The national average for gasoline hits a period low of $2.98 per gallon. Markets remain cautiously optimistic that regional conflicts in the Middle East will remain contained.

- Late February: Tensions involving Iran escalate significantly. Diplomatic efforts to secure long-term maritime security in the Persian Gulf encounter setbacks, leading to an immediate "war risk premium" being applied to crude oil futures.

- Early March: Reports of a potential two-week ceasefire emerge, briefly stabilizing oil prices. However, the ceasefire is characterized by frequent violations and a lack of formal enforcement, leading to renewed market skepticism.

- Mid-March: Disruptions in the Strait of Hormuz—a vital artery for global energy transit through which approximately 20% of the world’s oil consumption passes—begin to impact shipping schedules. Insurance premiums for tankers rise, adding to the landed cost of crude.

- Late March to April: The cumulative effect of these disruptions manifests at American gas stations. The national average surpasses the $4.00 mark, reaching $4.16 as the full weight of the March energy price surge is integrated into retail markets.

Analysts note that because economic data is inherently backward-looking, the CPI and PCE reports released in early April only partially capture the recent escalation. Much of the surge in oil and gas prices occurred in the latter half of March and continued into April, suggesting that the inflation reports for the second quarter may be even more concerning than those currently available.

Implications for Federal Reserve Monetary Policy

The persistence of inflation above the 2% target, compounded by rising energy costs, has profound implications for the Federal Reserve’s path regarding interest rates. For much of early 2024, investors had anticipated a series of rate cuts beginning in the summer. However, the "hideous" nature of the recent data, as described by some market observers, has forced a recalibration of these expectations.

Federal Reserve officials have consistently maintained that they require "greater confidence" that inflation is moving sustainably toward their target before they consider easing monetary policy. The recent surge in energy prices complicates this mission. If the Fed cuts rates while energy costs are pushing headline inflation higher, they risk a resurgence of price instability that could require even more aggressive tightening later. Consequently, the "higher-for-longer" narrative has gained significant traction. This policy stance implies that the federal funds rate may remain at its current restrictive levels well into the latter half of the year, or even into 2025, depending on the duration of the energy shock.

Higher interest rates exert pressure on various segments of the economy, particularly those that are capital-intensive or sensitive to borrowing costs. While the broader labor market has remained resilient, the prolonged period of elevated rates is beginning to expose vulnerabilities in corporate balance sheets and the commercial real estate sector.

Market Concentration and the Risk of a "Hidden Crash"

As the reality of sustained high interest rates sets in, the leadership of the equity markets is undergoing a subtle but critical shift. During periods of cheap money and low inflation, growth-oriented sectors—particularly "Big Tech"—tended to dominate market returns. However, historical precedents, such as the market cycle of the early 2000s, suggest that when the macroeconomic environment shifts toward higher inflation and rates, the previous winners often enter a period of prolonged stagnation.

Market analysts have raised concerns regarding the extreme concentration of investor capital in a handful of technology giants. While the major indices may appear stable on the surface, a "hidden crash" can occur when these dominant stocks stop providing gains, leading to years of flat or disappointing returns for investors who lack true diversification. As energy costs rise and interest rates remain elevated, capital is beginning to migrate away from overvalued tech stocks and toward "edge innovators"—companies that provide essential infrastructure, energy solutions, or commodities that are better positioned to thrive in an inflationary environment.

Broader Economic Outlook and Necessary Conditions for Normalization

For the U.S. economy to return to a state of price stability and predictable growth, several geopolitical and domestic factors must align. Foremost among these is the stabilization of energy transit routes. If traffic in the Strait of Hormuz returns to pre-conflict levels and negotiations between Western powers and Iran yield a more durable diplomatic framework, the uncertainty premium currently embedded in oil prices would likely dissipate.

Furthermore, the domestic economy must continue to navigate the transition from a period of stimulus-driven demand to one defined by fiscal and monetary restraint. The Federal Reserve’s ability to manage this transition depends heavily on external factors beyond its control, such as global supply chain integrity and international relations.

In conclusion, the recent inflation data serves as a sobering update for the American consumer and the global investor alike. While headline figures for February and March were in line with some expectations, the underlying trend—driven by a volatile energy sector—suggests that the battle against inflation is far from over. As long as geopolitical tensions keep energy costs elevated, the Federal Reserve will likely find its hands tied, keeping interest rates high and forcing a re-evaluation of investment strategies across the financial spectrum. The path forward requires a cautious approach, as the economy remains sensitive to every new headline from the world’s most volatile energy-producing regions.