Major Bank Earnings Signal Economic Resilience Amid Persistent Geopolitical and Inflationary Pressures

The arrival of the first-quarter earnings season for the banking sector has provided a critical data-driven pivot for global markets, offering a reprieve from the speculative atmosphere that has dominated investor sentiment for much of the year. For several weeks, financial markets have operated under a cloud of uncertainty, characterized by fluctuating oil prices, stubborn inflation data, and shifting expectations regarding the Federal Reserve’s timeline for interest rate reductions. This period of "geopolitical noise" has now been met with tangible financial metrics and forward-looking guidance from the nation’s largest lending institutions, serving as a bellwether for the broader health of the United States economy.

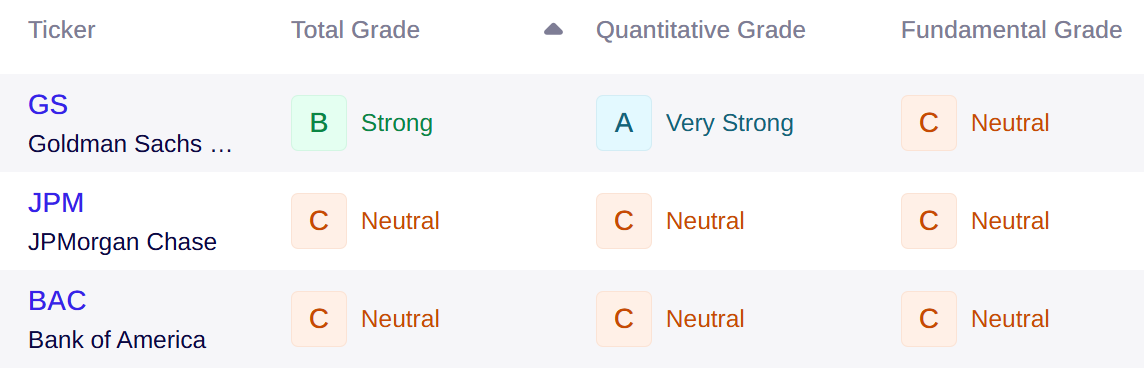

While financial reporting in the banking sector is often viewed with a degree of skepticism due to the complexity of institutional accounting and the flexibility of reporting standards, these early results offer an essential diagnostic of current economic conditions. The initial wave of reports from Goldman Sachs, JPMorgan Chase, and Bank of America suggests that while significant segments of the economy are performing better than analysts initially projected, there remain underlying vulnerabilities that necessitate a cautious outlook for the remainder of the fiscal year.

Goldman Sachs and the Resurgence of Investment Banking

The Goldman Sachs Group, Inc. (GS) opened the earnings week with a performance that exceeded consensus estimates, signaling a potential revival in the capital markets and deal-making sectors. The firm reported a 19% year-over-year increase in earnings, totaling $5.6 billion, or $17.55 per share. Total revenue for the quarter rose by 14% to $17.23 billion, surpassing the expectations of Wall Street analysts.

A granular analysis of the Goldman Sachs report reveals that the primary drivers of this growth were concentrated in its core strengths: equities trading and investment banking. The firm’s equities trading revenue reached a record $5.33 billion, marking a 27% increase. Furthermore, investment banking fees surged by 48% to $2.84 billion. These figures indicate a significant uptick in market activity and a willingness among corporate clients to engage in mergers, acquisitions, and equity offerings, despite the high-interest-rate environment.

However, the market reaction to these robust figures was notably muted. Shares of Goldman Sachs experienced a 2% decline following the announcement. Market observers suggest this reaction reflects concerns over the sustainability of trading-driven growth. Because trading and investment banking are inherently volatile and sensitive to market fluctuations, investors remain wary of whether this momentum can be maintained if geopolitical tensions or inflationary pressures trigger a broader market cooldown.

JPMorgan Chase and the Cautionary Guidance of Jamie Dimon

JPMorgan Chase & Co. (JPM), the largest bank in the United States by assets, also reported strong headline figures but paired them with a sober assessment of the future. The institution recorded a 13% increase in earnings, reaching $16.5 billion, or $5.94 per share. Total revenue climbed 10% to $50.54 billion, both of which topped analyst projections.

Key metrics within the report showed that fixed-income trading revenue rose by 21% to $7.08 billion, while investment banking fees grew by 28% to $2.88 billion. A positive indicator for the broader economy was the bank’s decision to set aside less capital for loan losses compared to previous quarters. This move suggests that borrowers are currently maintaining their repayment schedules and that consumer credit health remains relatively stable.

Despite these achievements, JPMorgan’s stock price faced downward pressure after the bank revised its 2026 net interest income (NII) guidance. The bank lowered its NII expectations from $104.5 billion to approximately $103 billion. CEO Jamie Dimon reinforced this cautious stance, highlighting "significant uncertainties" on the horizon. Dimon pointed toward persistent inflationary pressures, elevated asset prices, and the unpredictable nature of global geopolitical conflicts as potential headwinds. This "fortress balance sheet" philosophy, while historically successful for JPMorgan, appeared to weigh on investor sentiment, leading to a 2% dip in share value post-earnings.

Bank of America and the Resilience of the American Consumer

Bank of America Corporation (BAC) provided a different perspective on the economy, focusing on the strength of its retail and consumer divisions. The bank reported its highest earnings per share in nearly two decades, which rose 17% to $1.11. Total revenue for the quarter increased by 7.2% to $30.43 billion.

Unlike its peers, which relied heavily on trading and institutional fees, Bank of America’s growth was bolstered by its consumer business. CEO Brian Moynihan emphasized that consumer spending remains "solid" and that credit quality has stayed stable. This is a critical metric for the U.S. economy, as consumer spending accounts for approximately two-thirds of domestic economic activity. The bank’s ability to grow net interest income while maintaining a healthy loan portfolio suggested that the "higher for longer" interest rate environment has yet to significantly dampen consumer demand. Following the report, Bank of America shares rose approximately 2%, reflecting investor confidence in the stability of the consumer sector.

Chronology of Economic Pressures Leading into Q1 Earnings

To understand the significance of these earnings, one must look at the timeline of economic events leading up to the reports.

- January-February 2024: Market optimism was high as investors anticipated as many as six rate cuts from the Federal Reserve starting in March. Inflation appeared to be on a downward trajectory.

- March 2024: The Consumer Price Index (CPI) print came in higher than expected at 3.5%, marking the third consecutive month of "sticky" inflation. The Federal Reserve adjusted its "dot plot," signaling fewer rate cuts than the market had priced in.

- Late March – Early April 2024: Oil prices surged amid escalating tensions in the Middle East, sparking fears of a secondary inflationary spike. The 10-year Treasury yield rose above 4.5%, putting pressure on equity valuations.

- Mid-April 2024: The "Big Three" banks reported, shifting the focus from macroeconomic speculation to microeconomic reality.

This chronology illustrates why the banking sector’s performance is being scrutinized so heavily. The banks are the first to feel the effects of interest rate shifts and the first to see changes in how businesses and consumers manage their capital.

Comparative Data Analysis: NII and Credit Quality

A critical area of focus for analysts during this earnings cycle has been Net Interest Income (NII)—the difference between what banks earn on loans and what they pay out on deposits. As the Federal Reserve maintains elevated interest rates, the "deposit beta" (the rate at which banks must increase interest paid to depositors) has begun to catch up with the rates charged on loans.

| Metric | Goldman Sachs | JPMorgan Chase | Bank of America |

|---|---|---|---|

| Earnings Growth (YOY) | 19% | 13% | 17% |

| Revenue Growth (YOY) | 14% | 10% | 7.2% |

| Investment Banking Fees | +48% | +28% | +35% (approx) |

| Stock Reaction | -2% | -2% | +2% |

The divergence in stock performance highlights a shift in investor preference. While Goldman and JPMorgan benefited from volatile market activity (trading and fees), Bank of America’s success was rooted in the more "predictable" consumer sector. The reduction in loan loss provisions across the board is a quantitative signal that the much-feared "hard landing" recession has not yet materialized.

Broader Economic Implications and Market Outlook

The collective message from these earnings reports is one of cautious resilience. The U.S. economy is currently operating in a bifurcated state. On one hand, the institutional side of the economy—capital markets, trading, and corporate advisory—is thriving on the volatility created by global uncertainty. On the other hand, the retail side of the economy is managing the transition to a high-interest-rate environment with surprising durability.

However, the "fundamental grades" of these institutions remain a point of contention for quantitative analysts. While the nominal numbers are strong, the underlying quality of earnings is being questioned. Much of the recent profit growth is attributed to short-term market noise rather than long-term structural demand. For instance, the surge in investment banking fees is partly a result of a backlog of deals from 2023 finally being executed, rather than a new wave of organic economic expansion.

Furthermore, the banking sector serves as a reminder of the "Hidden Crash" occurring in specific market segments. While large-cap indices remain near all-time highs, many interest-rate-sensitive sectors, such as small-cap stocks and commercial real estate, continue to struggle. The banks’ cautious guidance on NII suggests they are preparing for a scenario where interest rates remain high for a longer duration than the market currently expects, which could eventually put more pressure on loan demand and credit quality.

Conclusion: The Path Forward for Investors

As the first-quarter earnings season continues to unfold, the focus will shift from the financial giants to the technology and industrial sectors. The data provided by the banking industry suggests that the "fog of war" is lifting, revealing an economy that is sturdy but slowing. Investors are now tasked with distinguishing between companies that are merely benefiting from market volatility and those with genuine earnings momentum and fundamental strength.

The lessons from Goldman Sachs, JPMorgan, and Bank of America are clear: the consumer is still spending, the markets are still active, but the margin for error is narrowing. With inflation remaining above the Federal Reserve’s 2% target and geopolitical risks showing no signs of abating, the transition from speculative growth to quality-driven investment will likely be the defining theme of the 2024 market. The banking sector has provided the first chapter of this narrative, and while the results are solid, the cautious tone from industry leaders suggests that the most challenging part of the economic cycle may still lie ahead.