Oracle Corp Expansion into AI Infrastructure Faces Financial Headwinds Amid Massive Capital Expenditure and Low Data Center Margins

Oracle Corp. (ORCL) has intensified its strategic pivot toward artificial intelligence infrastructure, marked by a significant expansion of its partnership with Bloom Energy Corp. (BE). The software giant recently reached an agreement to purchase up to 2.8 gigawatts (GW) of fuel cell power from Bloom Energy, a substantial increase over the 1.2 GW already under contract. This deal, aimed at securing on-site power generation for Oracle’s rapidly expanding data center footprint, triggered a notable surge in market activity. Oracle’s shares climbed 13% on the Monday following the announcement, followed by a further 4% gain on Tuesday, while Bloom Energy saw its stock price appreciate by 22%.

Under the terms of the expanded agreement, Oracle is positioning itself to mitigate the growing energy constraints facing the global data center industry. The fuel cells provided by Bloom Energy will support the electricity-intensive demands of AI training and inference. To facilitate the partnership, Bloom Energy has issued a warrant allowing Oracle to purchase 3.53 million shares of BE stock at a strike price of $113.28 per share. Should Oracle exercise this warrant, the total investment would amount to approximately $400 million. While the deal underscores Oracle’s commitment to the AI sector, it also highlights the escalating costs associated with the company’s infrastructure-heavy strategy.

Chronology of Capital Expenditure Escalation

Oracle’s transition from a high-margin software provider to a capital-intensive cloud and AI infrastructure player has been characterized by a rapid and unprecedented increase in planned spending. This shift is reflected in the company’s capital expenditure (CapEx) guidance over the past eighteen months. In early 2023, Oracle management projected a CapEx budget of $16 billion for the 2026 fiscal year. However, as the global demand for AI processing power surged, the company repeatedly revised these figures upward.

By mid-2023, the guidance was increased to $25 billion. In September of the same year, the figure rose to $35 billion, and by December, management indicated that CapEx could reach $50 billion. This aggressive spending trajectory is intended to fund the construction and outfitting of "hyperscale" data centers capable of hosting the massive GPU clusters required for modern large language models (LLMs). The acceleration in spending represents a fundamental change in Oracle’s business model, moving the company into direct competition with established hyperscalers such as Amazon Web Services (AWS), Microsoft Azure, and Google Cloud.

Financial Stability and the Debt Burden

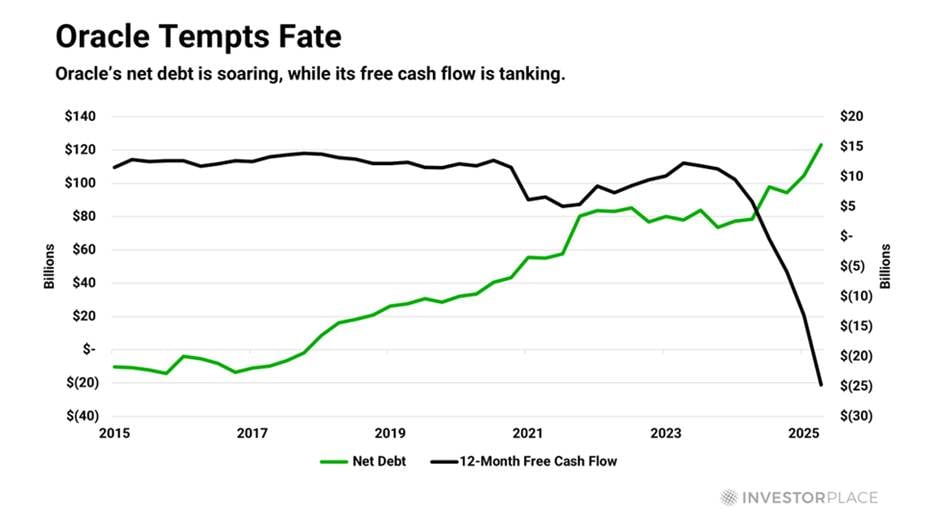

The massive scale of Oracle’s AI ambitions has placed a visible strain on its corporate balance sheet. As of the most recent fiscal reports, Oracle carries a net debt and lease liability total of approximately $120 billion. This leverage is particularly notable given the current interest rate environment, which has increased the cost of servicing long-term debt. Furthermore, in fiscal 2025, Oracle reported negative free cash flow for the first time since 1990. This metric is a critical indicator of a company’s ability to fund operations and expansion without relying on external financing or depleting cash reserves.

The reliance on debt to fund infrastructure has raised questions among some analysts regarding the long-term sustainability of Oracle’s capital structure. While the company has historically generated robust cash flows from its legacy database and software-as-a-service (SaaS) businesses, the transition to infrastructure-as-a-service (IaaS) requires continuous, heavy investment in physical assets that depreciate over time. The contrast between the asset-light software business and the asset-heavy data center business is a central theme in the current evaluation of Oracle’s financial health.

Margin Compression and Operational Challenges

One of the primary concerns surrounding Oracle’s AI pivot is the disparity in profit margins between its traditional business lines and its new infrastructure ventures. Oracle’s legacy software business has historically enjoyed gross margins exceeding 80%, a hallmark of the enterprise software industry. In contrast, the data center business is far more operationally expensive.

While Oracle management has guided investors toward expected gross margins of 30% to 40% for its AI data centers, internal documents suggest the reality may be more challenging. Reports indicate that Oracle’s AI data center operations have recently averaged gross margins as low as 16%. To put this into perspective, traditional brick-and-mortar retailers like Walmart Inc. (WMT) operate with gross margins of approximately 24%. The low margin profile of AI infrastructure suggests that Oracle must achieve massive scale and operational efficiency to justify the high level of capital investment.

The lower margins are attributed to several factors, including the high cost of specialized AI hardware—primarily NVIDIA GPUs—and the escalating costs of electricity and cooling. By investing in on-site power through Bloom Energy, Oracle is attempting to bypass the volatility and capacity limits of the public electrical grid, but this independence comes with its own upfront capital costs.

The OpenAI Dependency and Tenant Risk

A significant portion of Oracle’s current AI momentum is tied to a single, high-profile customer: OpenAI. Market data suggests that roughly 60% of Oracle’s contracted backlog for AI capacity is attributed to OpenAI. This concentration of revenue creates a "tenant risk" that is uncommon in more diversified cloud environments.

OpenAI, while a leader in the generative AI space, remains a private entity that is heavily dependent on external funding and its partnership with Microsoft. If OpenAI were to face a decline in market share, a funding shortfall, or a shift in its infrastructure strategy, Oracle could find itself with significant underutilized capacity. Oracle currently faces approximately $248 billion in long-term lease obligations for data centers. If the primary tenant for these facilities cannot sustain its growth or payments, Oracle’s financial exposure would be substantial. This dynamic has led some observers to characterize Oracle’s strategy as a high-stakes bet on the continued dominance of a single AI developer.

Historical Context: Parallels to the Dot-Com Era

The current fervor surrounding AI infrastructure has drawn comparisons to the telecommunications and internet build-out of the late 1990s. During the dot-com bubble, companies invested billions of dollars in fiber-optic networks and early data centers, driven by projections of exponential internet growth. When the bubble burst in March 2000, many of these companies were left with "dark fiber" and empty facilities, leading to a decade of consolidation and bankruptcies.

At the peak of the dot-com era, the Nasdaq-100 index traded at approximately 81 times earnings. While Oracle’s current valuation is not at those historical extremes, the "new era" narrative—the idea that traditional financial metrics no longer apply because of a revolutionary technology—is once again prevalent. Analysts note that while the technology (AI) is undeniably transformative, the economic reality of building the hardware to support it remains subject to the laws of supply, demand, and capital returns. Historically, sectors like energy, healthcare, and commodities have often outperformed high-growth tech following periods of extreme valuation expansion, a trend that some investors are monitoring as they weigh the risks of Oracle’s current trajectory.

Market Sentiment and Analyst Perspectives

Despite the financial risks and margin pressures, the prevailing sentiment on Wall Street remains largely positive. Of the 50 analysts who actively cover Oracle, 40 maintain a "Buy" rating. This optimism is fueled by the belief that AI represents a multi-generational shift in enterprise computing and that Oracle’s established relationships with large corporations give it a unique advantage in deploying AI solutions.

Proponents of the stock argue that the current CapEx surge is a necessary "entry fee" to compete in the next era of technology. They suggest that once the initial infrastructure is built, Oracle will be able to layer high-margin software services on top of its cloud platform, eventually restoring its overall margin profile. However, a minority of analysts remain cautious, pointing to the insider selling activity observed at Oracle over the past year and the company’s high debt-to-equity ratio.

Broader Impact and Industry Implications

Oracle’s move to secure 2.8 GW of power is a bellwether for the broader technology industry. It highlights a critical bottleneck in the AI revolution: energy. As data centers consume an increasing share of the global power supply, the ability to generate electricity on-site—independent of the grid—is becoming a competitive necessity.

The partnership with Bloom Energy may signal a shift in how hyperscalers approach utility management. If Oracle’s fuel cell strategy proves successful, it could force competitors like Amazon and Google to pursue similar decentralized energy solutions, potentially disrupting the traditional utility business model.

In conclusion, Oracle Corp. is currently engaged in one of the most ambitious and capital-intensive transformations in its history. By betting heavily on AI infrastructure and securing massive energy resources, the company is positioning itself at the center of the next technological wave. However, the path is fraught with financial challenges, including mountainous debt, negative free cash flow, and thin operational margins. Whether Oracle can successfully navigate these headwinds or if the cost of its ambition will lead to long-term financial instability remains a central question for the global markets. The company’s performance over the coming fiscal years will serve as a definitive case study on the viability of the "infrastructure-first" approach to the artificial intelligence economy.