Analysis of Inflation Data Energy Market Volatility and the Federal Reserve’s Monetary Outlook

The economic landscape of the United States has reached a critical juncture as recent data from June reveals a significant cooling in inflationary pressures, primarily driven by a sharp reversal in energy costs. For many observers, the current volatility in the energy sector evokes memories of the October 1973 energy crisis, when conflict in the Middle East led to an Arab oil embargo that fundamentally altered the American economy. During that era, gasoline supplies tightened to the point of scarcity, and prices soared, forcing drivers into lines that spanned city blocks. Inflation ceased to be a theoretical metric and became a visible, daily struggle manifested in gas station signage and depleted family budgets. While the modern economy is more diversified than it was fifty years ago, the recent eruption of hostilities in the Middle East initially threatened to trigger a similar feedback loop of rising crude prices and systemic inflation.

However, the narrative shifted significantly by the end of the second quarter. After an initial surge, oil prices underwent a notable retreat, with crude returning toward pre-conflict levels by late June. This reversal has been a primary catalyst for the latest cooling in both the Consumer Price Index (CPI) and the Producer Price Index (PPI), offering a reprieve to consumers and providing the Federal Reserve with more flexibility in its monetary policy. Despite this progress, analysts remain cautious, noting that while the headline numbers are encouraging, the underlying volatility of energy markets remains a "wild card" that could influence economic stability through the remainder of the year.

A Chronology of Energy Volatility and Market Reaction

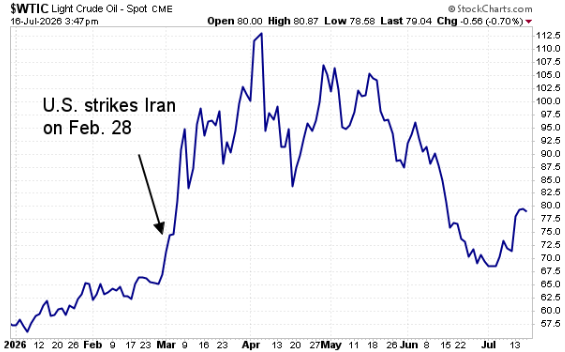

The relationship between geopolitical instability and domestic inflation has been starkly illustrated over the past several months. When war broke out in the Middle East earlier this year, West Texas Intermediate (WTI) crude oil prices responded with immediate upward pressure. This followed a historical pattern where fears of supply chain disruptions in the Strait of Hormuz—a vital artery for global oil transit—lead to speculative buying and increased insurance premiums for cargo.

By May, the Producer Price Index reflected this tension, with wholesale prices jumping 1.1%, largely on the back of surging energy costs. At that time, fears were mounting that the Federal Reserve might be forced to consider further interest rate hikes to prevent a second wave of inflation from taking root. However, as the weeks progressed into June, the expected long-term disruptions did not materialize to the degree initially feared. Global energy markets proved resilient as alternative shipping routes and increased production from non-OPEC sources helped stabilize supply.

By late June, the initial price spike in crude oil had largely been erased. This shift was immediately reflected in the June inflation reports, which showed that the "energy shock" had transitioned into a "disinflationary tailwind." This rapid reversal underscores the difficulty of timing market entries and exits based solely on geopolitical headlines, as the fundamental drivers of supply and demand often reassert themselves once initial panic subsides.

The June Consumer Price Index: A Significant Cooldown

The June CPI report provided the most substantial evidence to date that the inflationary surge of the post-pandemic era is losing momentum. Consumer prices fell by 0.4% on a monthly basis in June, marking the first such decline since 2020. This figure was notably better than the 0.2% decline anticipated by consensus economic forecasts. On an annual basis, the inflation rate cooled to 3.5%, a significant drop from the 4.2% recorded in May and well below the 3.8% forecast.

A granular look at the CPI components reveals the specific drivers of this decline:

- Gasoline Prices: The most significant contributor to the monthly drop was a 9.7% decrease in gasoline prices, directly tracking the retreat in global oil prices.

- Core CPI: Excluding the volatile food and energy sectors, Core CPI remained unchanged for the month. This brought the annual core rate down to 2.6%, compared to 2.9% in the previous month.

- Housing and Rent: One of the most encouraging data points for the Federal Reserve was the modest 0.2% rise in "owners’ equivalent rent." As housing costs represent a significant portion of the CPI basket and have remained stubbornly high for years, this softening suggests that the lag in shelter inflation is finally catching up with real-world market cooling.

- Food Prices: Food costs saw a marginal increase of 0.2%, indicating that while grocery bills are not falling, the rate of increase has stabilized to a level consistent with long-term averages.

Producer Price Index Confirms Wholesale Relief

The cooling trend was further validated by the release of the Producer Price Index (PPI), which measures the prices received by domestic producers for their output. Producer prices fell by 0.3% in June, outperforming expectations of a flat reading. This represented the first monthly decline in wholesale prices since August of the previous year.

On an annual basis, PPI growth slowed to 5.5%, down from 6.0% in May. Within the report, energy prices showed a steep monthly decline of 6.4%, while food prices slipped 0.6%. The Core PPI, which excludes food and energy, rose by a modest 0.2%, suggesting that inflationary pressures at the production level are becoming increasingly contained. Because producer prices often serve as a leading indicator for consumer prices—as costs incurred by manufacturers are eventually passed down to the retail level—the June PPI report suggests that the "pipeline" for inflation is clearing.

The Federal Reserve and the Interest Rate Outlook

The convergence of lower-than-expected CPI and PPI data has fundamentally shifted the conversation regarding the Federal Reserve’s next moves. Throughout the first half of the year, Federal Reserve officials maintained a "higher for longer" stance, wary of cutting interest rates prematurely and risking a resurgence of price growth.

However, the June data has effectively removed the threat of further rate hikes from the immediate horizon. With inflation moving closer to the Fed’s 2% long-term target and market interest rates already beginning to trend lower, the focus has shifted toward the timing of the first rate cut. Analysts suggest that if housing costs continue to stabilize and energy prices do not experience another major shock, the central bank may find the "goldilocks" scenario it has been seeking: a soft landing where inflation is tamed without triggering a deep recession.

Energy as the Persistent Wild Card

Despite the optimism surrounding the June reports, energy remains a volatile variable. While WTI crude prices fell back toward the $70 mark in June, they have recently shown signs of firming up again. Historically, energy demand peaks during the summer months due to increased travel, a trend often referred to as the "driving season" which concludes around Labor Day.

Furthermore, the geopolitical situation in the Middle East remains fluid. Any escalation that threatens the actual flow of oil—rather than just the sentiment surrounding it—could quickly reverse the progress made in June. Economists warn that while the current numbers are a victory for the "disinflation" narrative, victory cannot be declared until the core components of the economy show sustained stability independent of fluctuating oil barrels.

Strategic Implications for Investors

The rapid shifts in the inflation narrative provide a vital lesson for market participants: economic reports are inherently retrospective, while markets are forward-looking. Chasing headlines regarding geopolitical strife or monthly government data can often lead to "whipsaw" effects, where investors buy at the peak of fear and sell at the trough of relief.

A more disciplined approach focuses on corporate fundamentals—specifically earnings growth, sales acceleration, and forward guidance. History shows that companies with superior fundamentals are best positioned to navigate periods of macroeconomic uncertainty. For instance, institutional buying patterns often gravitate toward sectors that benefit from technological shifts or essential services, regardless of the broader inflationary environment.

An analysis of top-performing assets over the past two years reveals that leadership has come from diverse sectors, including:

- Artificial Intelligence and Hardware: Companies specializing in AI servers and chip manufacturing have seen gains exceeding 300% to 600% as the infrastructure for the next industrial revolution is built.

- Energy Infrastructure: Despite price volatility, offshore energy services and power plant construction firms have posted returns in the 270% range, driven by long-term global energy needs.

- FinTech and Payments: "Buy now, pay later" platforms have surged by over 700% since late 2024, reflecting shifts in consumer credit behavior.

- Precious Metals: Gold and strategic mineral miners have provided a hedge against currency devaluation, with many posting gains above 100%.

These results suggest that while inflation and Federal Reserve policy create the "weather" of the market, individual company performance provides the "climate." Investors who prioritize fundamentally strong companies with institutional support tend to outperform those who react to every swing in the CPI.

Conclusion and Future Outlook

As the third quarter progresses, the primary focus for the U.S. economy will be whether the June "cool down" was a temporary anomaly or the start of a sustained trend. The Federal Reserve will be looking for continued moderation in the services sector and shelter costs to confirm that the inflationary cycle has truly broken.

For the consumer, the immediate relief at the gas pump and the stabilization of grocery prices provide a much-needed increase in purchasing power. However, with energy prices remaining sensitive to global events, the path to the Fed’s 2% target remains fraught with potential obstacles. The coming months through Labor Day will be a testing ground for the resilience of the American economy and the permanence of the current disinflationary trend. For now, the data suggests a move in the right direction, but vigilance remains the watchword for policymakers and investors alike.