The Federal Reserve concluded its March policy meeting today, electing to maintain the federal funds rate at a target range of 3.50% to 3.75%. The decision, which was widely anticipated by institutional analysts and economists, signals a continued period of observation for the central bank as it navigates a complex landscape of persistent inflation, shifting labor dynamics, and heightening geopolitical volatility. While the hold itself was expected, the Federal Open Market Committee (FOMC) and Chairman Jerome Powell delivered a message defined by caution, emphasizing that the path forward remains obscured by significant economic and global unknowns.

Federal Reserve Policy and the Summary of Economic Projections

The March meeting provided an updated Summary of Economic Projections (SEP), offering a glimpse into the internal expectations of policymakers. While the benchmark rate remains unchanged, the underlying data suggests a central bank that is in no rush to implement the rate cuts that many market participants had hoped for earlier in the year. The Fed’s cautious stance is rooted in a desire to ensure that inflation is durably moving toward its 2% target before loosening financial conditions.

Chairman Powell’s press conference was notable for its frequent use of the word "uncertainty." This rhetorical shift suggests that the "soft landing" narrative, while still possible, is facing new headwinds. Legendary investor Louis Navellier, providing analysis in a recent flash alert, characterized the Fed’s tone as "vague," noting that the official statement acknowledged low job gains and the unpredictable fallout from ongoing conflicts in the Middle East. According to Navellier, the central bank’s language regarding the implications of Middle Eastern developments on the U.S. economy indicates a lack of clarity within the FOMC regarding near-term global impacts.

Despite characterizing the U.S. economy as "solid," Powell’s commentary lacked the definitive confidence required to soothe a jittery market. The combination of a resilient but uneven economy, stubborn inflation, and rising external risks has effectively locked the Fed into a "wait-and-see" posture, leaving investors to grapple with the reality of higher-for-longer interest rates.

Market Reaction and Geopolitical Catalysts

The financial markets responded negatively to the Fed’s lack of a clear timeline for rate reductions. All three major U.S. indexes closed the trading session down by more than 1%. The Dow Jones Industrial Average saw the steepest decline, falling 1.63%, while the S&P 500 and the Nasdaq Composite followed suit.

However, the Federal Reserve’s announcement was not the sole driver of today’s sell-off. Market sentiment was further dampened by a sharp surge in natural gas prices following reports of an attack by Iranian forces on a major liquefied natural gas (LNG) facility in Qatar. This escalation in the Gulf region has sparked immediate concerns regarding the security of energy infrastructure in one of the world’s most critical export hubs. The threat of sustained higher energy prices presents a dual challenge for the Fed: it acts as a tax on consumers, potentially slowing growth, while simultaneously exerting upward pressure on headline inflation.

The AI Infrastructure Cycle: A Parallel Economic Engine

While much of the broader market remains tethered to the Federal Reserve’s every move, a significant segment of the technology sector appears to be operating under a different set of economic rules. The massive buildout of Artificial Intelligence (AI) infrastructure is currently functioning as an independent capital cycle, largely insulated from incremental changes in interest rates.

Recent data from Bloomberg highlights the scale of this phenomenon. The four largest U.S. technology "hyperscalers"—Alphabet Inc., Amazon.com Inc., Meta Platforms Inc., and Microsoft Corp.—are projected to reach a combined capital expenditure of approximately $650 billion by 2026. This level of spending is intended to fund the construction of massive data centers and the procurement of high-performance computing hardware.

This "boom without parallel this century" is driven by strategic necessity rather than cheap liquidity. These corporations are making multi-year bets on the transformative power of AI, viewing the infrastructure buildout as a foundational requirement for future competitiveness. Because these investments are viewed as essential, they are less sensitive to the cost of borrowing than traditional industrial or consumer-facing sectors. This creates a "capital cycle" driven by technological demand, operating outside the traditional economic playbook that the Fed uses to manage the broader economy.

Red Flags in Private Credit and Software Lending

Despite the massive inflows into AI infrastructure, other areas of the technology and financial ecosystem are showing signs of significant distress. A primary area of concern is the private credit market, which has grown rapidly over the last several years as a primary source of funding for software-as-a-service (SaaS) companies and mid-market enterprises.

Morgan Stanley recently issued a warning regarding the health of direct lending portfolios. Analysts at the bank expect default rates in private credit to climb toward 8%, a level approaching the peaks seen during the COVID-19 pandemic. This stress is particularly evident in firms with heavy exposure to the software sector. Many of these loans were underwritten based on the assumption of high, recurring revenue growth and stable interest rates—assumptions that are now being challenged.

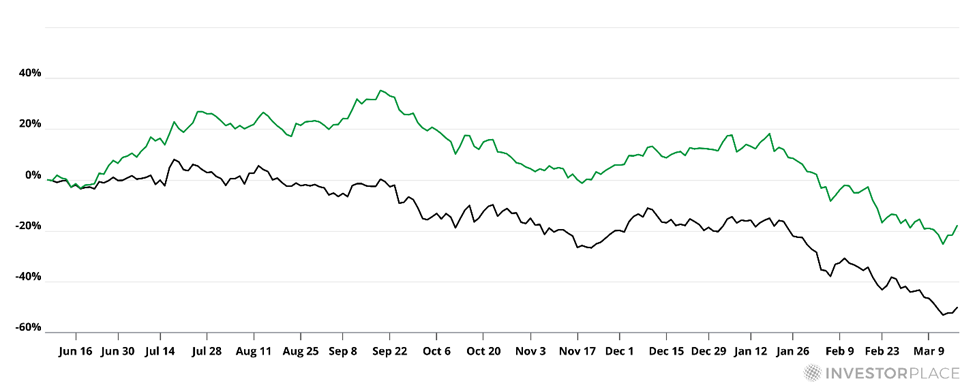

Specific institutional players are already feeling the impact of this shift. Blue Owl Capital (OWL) and Blackstone (BX) have seen their stock prices come under significant pressure this year. Since initial warnings were issued in mid-2025, Blackstone has lost 20% of its value, while Blue Owl Capital has experienced a 50% decline. The downturn reflects growing investor anxiety over the quality of their underlying loan portfolios and the potential for a wave of defaults as borrowing costs remain elevated.

Furthermore, the software industry itself is facing a structural threat from the very AI technology it seeks to integrate. AI is increasingly capable of automating complex workflows that were previously the primary revenue drivers for traditional software firms. A prominent example is Adobe (ADBE), which has seen its stock price drop 54% since August 2024. As AI systems begin to handle creative and administrative tasks autonomously, the traditional "per-seat" licensing models of many software companies are becoming vulnerable, raising questions about their long-term ability to service the debt held by private credit lenders.

Identifying AI Bottlenecks: Where the Money is Flowing

For investors looking to navigate this environment, the strategy of "following the money" has led to the identification of specific bottlenecks within the AI supply chain. As the initial rush for computing power (GPUs) matures, new constraints are emerging where demand significantly exceeds supply. These bottlenecks represent the areas where capital is most likely to generate outsized returns.

- Copper and Raw Materials: Copper is a critical component in the expansion of data centers, power grids, and cooling systems. The sheer volume of electrical infrastructure required to support AI processing has led to a surge in demand for high-quality copper, even as global mining output struggles to keep pace.

- Advanced Memory: AI models require massive amounts of high-speed memory to process datasets. As chips become faster, the memory bottleneck has become a primary constraint for hardware manufacturers, making advanced memory providers essential players in the ecosystem.

- Energy and Power Infrastructure: Perhaps the most significant bottleneck is energy. Data centers are incredibly power-hungry, and the existing electrical grid in many regions is reaching capacity. Companies involved in energy generation, grid modernization, and innovative cooling solutions are seeing unprecedented demand as hyperscalers scramble to secure the power necessary to keep their AI systems running.

Macro investing experts, including Eric Fry, have noted that these supply constraints are where the "imbalance" is most pronounced. In a recent analysis, Fry highlighted 15 companies positioned across these emerging constraints, spanning raw materials, energy infrastructure, and memory technology. These firms are effectively the "gatekeepers" of the AI buildout, as their products and services are required for the next phase of technological expansion.

Broader Economic Implications and the Path Ahead

The current economic landscape is characterized by a stark divergence. On one hand, the Federal Reserve is managing a traditional economy that is slowing under the weight of restrictive policy and geopolitical shocks. On the other hand, a massive, self-funded technological revolution is moving forward at an accelerated pace, consuming vast amounts of capital and resources.

This is not "stagflation" in the traditional sense, as Chairman Powell was careful to note, but it is a period of "unusual uncertainty" that complicates the outlook for broad market indexes. While the Fed remains cautious, the AI infrastructure cycle continues to create pockets of immense opportunity, particularly in the commodities and infrastructure sectors that serve as the backbone of the digital age.

As the market enters the second quarter of the year, investors must distinguish between companies that are reliant on Fed-driven liquidity and those that are essential to the structural shifts occurring in the global economy. With private credit defaults rising and energy security back in the spotlight, the "steady" economy described by the Fed may hide deeper fractures that will require careful navigation in the months to come.